A structured, obligation-based formula for calculating exactly how much life insurance your family needs — trusted by financial planners worldwide.

The DIME method is a four-part framework used by financial advisors to estimate life insurance needs. Instead of vague rules of thumb like "10× your salary," DIME calculates a precise number anchored to your real financial obligations.

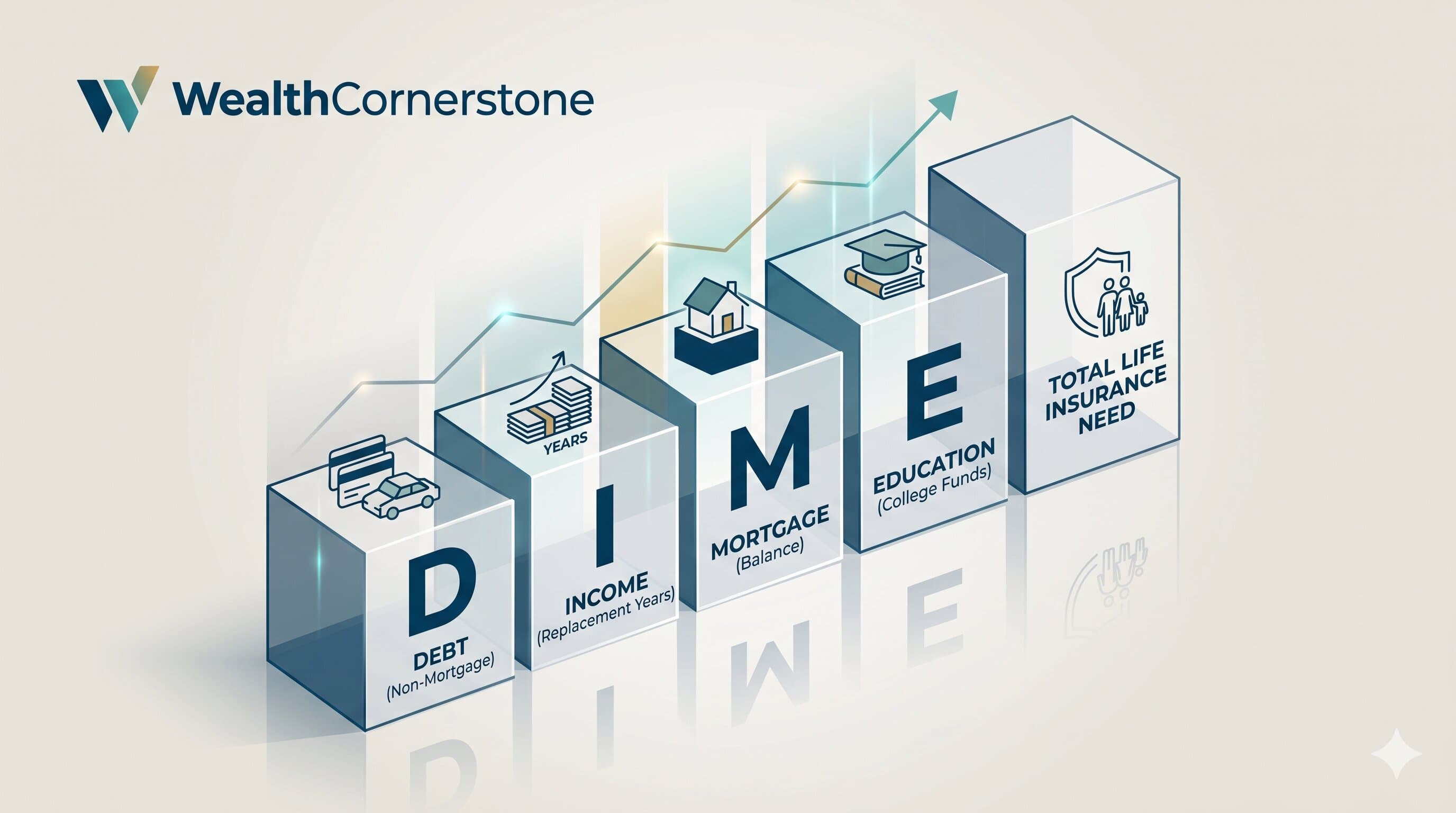

The Four Components

D — Debt

All outstanding non-mortgage debt: car loans, student loans, credit card balances, personal loans. If you die unexpectedly, these obligations don't disappear — they fall to your estate and your family. Including them in your coverage ensures they're paid off without depleting savings.

I — Income

The largest component for most families. Rather than a simple multiply, income is compounded by inflation each year — because $100,000 today is worth less in 10 years. This replaces the real purchasing power of your paycheck, not just the nominal number.

M — Mortgage

The outstanding principal balance on your home loan. Paying off the mortgage means your family keeps the house without a monthly burden. Choose full payoff or fund a set number of years of payments.

E — Education

Projected college costs for all your children, inflated at 6% per year from today to each child's 18th birthday. Any existing 529 savings are subtracted, so you're covering the actual gap — not double-counting what you've already set aside.

Why DIME Matters

Most people either underinsure — leaving their family financially exposed — or overinsure, paying premiums they don't need. Both are costly mistakes.

DIME anchors your coverage to real numbers: your actual debt, your inflation-adjusted income stream, your actual mortgage balance, and your children's actual education timeline. The result is specific to your household.

Key benefits of the DIME method:

- Eliminates guesswork with a structured four-part formula

- Inflation-adjusts income so future dollars aren't overstated

- Easy to recalculate after major life events (new child, new home, pay rise)

- Recognized and used by CFPs and insurance professionals

- Works for single-income and dual-income households

Worked Example

Profile: 38-year-old, two children (ages 5 and 9), $400,000 mortgage, $60,000 annual income — using 3% inflation and 15 years of replacement income.

| Component | Calculation | Amount |

|---|---|---|

| D — Debt | Car + student + credit card | $45,000 |

| I — Income | $60,000 compounded at 3% × 15 yrs | $1,082,369 |

| M — Mortgage | Outstanding balance | $400,000 |

| E — Education (child 1, age 5) | $80,000 × 1.06^13 | $170,437 |

| E — Education (child 2, age 9) | $80,000 × 1.06^9 | $135,128 |

| Emergency Fund | $4,500 × 6 months | $27,000 |

| Total Insurance Need | $1,859,934 |

With $500,000 existing coverage, the gap is $1,359,934 — a significant underinsurance risk.

Note: income of $60,000 compounded at 3% for 15 years sums to ~$1.08M — substantially more than the simple $60k × 15 = $900k estimate.

Strengths & Limitations

Strengths

- Easy to understand and communicate

- Covers all major financial obligations

- Produces a concrete, actionable number

- Inflation-adjusts income for accuracy

- Adaptable to any family structure

Limitations

- Doesn't account for Social Security survivor benefits

- Ignores investment growth on existing assets

- Doesn't model spouse's income

- Best used as a starting point, not final advice

Get Your Number

Ready to calculate your coverage need? Our free calculator uses the full DIME method with inflation-adjusted income — takes under 2 minutes and requires no sign-up. Use it today to discover if you're properly protected.

Frequently Asked Questions

Does the DIME method account for Social Security survivor benefits?

No — and that is intentional. DIME calculates the gross insurance need before subtracting any expected Social Security benefits, because survivor benefit amounts vary significantly by age, earnings history, and family structure. A financial advisor can help you subtract your estimated Social Security survivor benefit from the DIME total to arrive at a net coverage number. Using the gross DIME figure is the conservative, safer default.

How often should I recalculate my DIME number?

Recalculate after any major life event: a new child, a home purchase or refinance, a significant raise or income change, a 529 contribution milestone, or paying off a major debt. As a baseline, running the calculation every 2–3 years catches drift even without a triggering event. Your DIME number can change by six figures from a single refinance or pay increase.

Can I use the DIME method if I am single with no dependents?

Yes, but the calculation simplifies considerably. Without income replacement for dependents and without education costs, your DIME total will primarily reflect outstanding debts (D) and possibly a mortgage (M). Single people often find DIME produces a lower number than they expected — which is useful, because it helps avoid over-insuring. Focus on the D and M components and add a small buffer for final expenses and estate settlement costs.

Is the DIME method recognized by insurance companies or the CFP Board?

The DIME method is not a licensed or regulated standard — it is a planning framework used by financial educators and independent advisors. Insurance companies use their own proprietary needs-analysis tools, which may produce different results. DIME is best understood as a structured starting point for your own calculation, not a binding industry formula. Always verify your coverage target with a licensed professional before purchasing a policy.

Further Reading

- What Is a Financial Safety Net and How to Build One — insurance is one pillar; see how it fits the complete safety net picture.

- How to Choose and Update Your Beneficiaries — once you know your coverage number, naming the right beneficiary is the next step.

- What Is Estate Planning and Why It Matters — life insurance works alongside a will and trust to protect your family completely.